Quarterly market outlook – second quarter 2025

Our investment strategists provide Edward Jones’ perspective on the economy and the markets, and what it may mean for your portfolio.

Past performance does not guarantee future results. An index is unmanaged and is not available for direct investment.

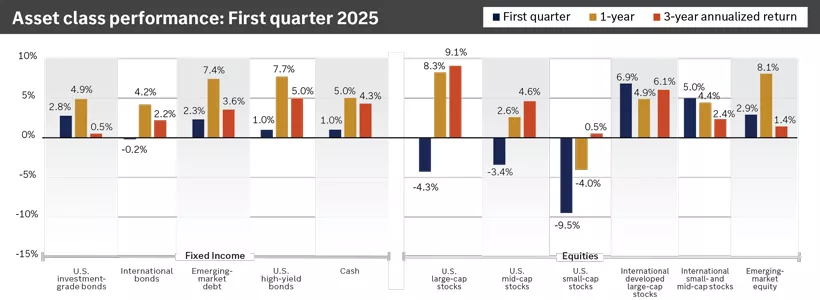

This chart shows first-quarter returns and three-year annualized returns in the fixed-income and equity markets.

Past performance does not guarantee future results. An index is unmanaged and is not available for direct investment.

This chart shows first-quarter returns and three-year annualized returns in the fixed-income and equity markets.

Looking back at the first quarter

Diversification showed its merit in Q1, with international equities and most fixed-income investments finishing higher despite volatility in U.S. equity markets.

Policy uncertainty weighed on U.S. equities

U.S. equities finished lower in Q1, marking the first quarterly decline in the S&P 500 since Q3 2023. Tariff uncertainty was a key driver of U.S. equity market volatility, as the U.S. proposed 25% tariffs on goods imported from Canada and Mexico before ultimately delaying the tariffs. The U.S. did, however, impose targeted tariffs on steel, aluminum and auto imports, as well as a 20% tariff on goods imported from China.

The uncertainty around tariffs weighed on sentiment in U.S. markets, with each of our recommended U.S. equity asset classes finishing lower. Growth-oriented sectors such as technology and consumer discretionary were among the laggards, while value-oriented sectors such as energy and health care were the top performers.

Expansionary fiscal policy boosted international stocks

International developed large-cap stocks outperformed in Q1, driven by strong performance in European stocks.

Policymakers in Germany passed legislation that will allow for higher fiscal spending on defense and infrastructure, boosting sentiment for the region. International developed large-cap stocks surged in response, outperforming U.S. large-cap stocks by over 11% and marking the largest quarterly margin of outperformance since 2002.

In addition, Chinese tech stocks rallied, providing a boost to emerging-market stock returns following the DeepSeek AI breakthrough in January.

Bonds provided stability to well-diversified portfolios

Bonds were mostly higher in Q1, aided by a pullback in yields as markets adjusted to expectations for potentially moderating economic growth. Additionally, the Federal Reserve announced at its March meeting that it plans to slow the pace of quantitative tightening, while updated projections showed policymakers still foresee two interest rate cuts in 2025, supporting the move lower in bond yields.

U.S. investment-grade bonds and emerging-market debt outperformed, gaining over 2%.

Action for investors

Broadening leadership beyond U.S. equities was on display in Q1, rewarding those with well-diversified portfolios. Talk with your financial advisor to ensure your portfolio is appropriately diversified based on your financial goals.

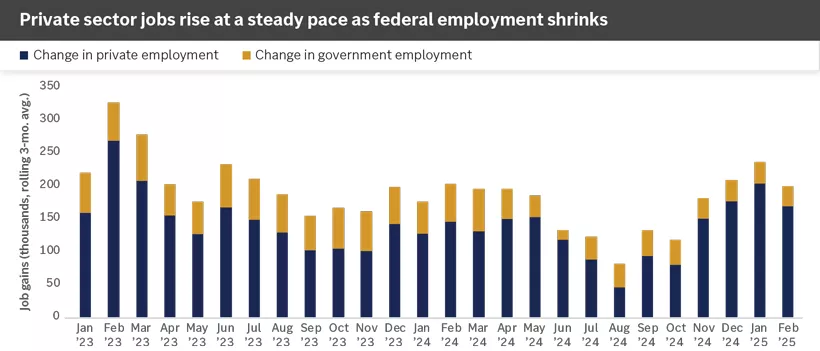

This chart illustrates changes in private sector and government employment from January 2023 through February 2025.

This chart illustrates changes in private sector and government employment from January 2023 through February 2025.

Economic outlook

Growth concerns have taken some wind out of the market’s sails, and high economic uncertainty is negatively impacting sentiment. Following a weak start to the year, a rebound in gross domestic product (GDP) and a shift to pro-growth policies should help sustain the expansion, though at a slower pace compared to last year.

Economy hits a soft patch in Q1

After growing at an above-trend 2.8% pace in 2024, the U.S. economy appears to have hit a speedbump in Q1. Increased trade policy uncertainty has negatively impacted consumer sentiment, while winter storms in parts of the country also likely depressed activity.

Additionally, a surge in imports will likely be a major drag in first-quarter GDP as U.S. companies sought to front-run any new tariffs. But growth should rebound in Q2 as this effect reverses, with imports slowing relative to exports.

Agenda may shift to pro-growth policies

So far this year, the focus has been on trade and efforts to constrain government spending. However, following the April tariff announcements, the administration may start shifting its attention to more market-friendly policies, which are taking longer to implement.

Pro-growth policies, such as tax cuts and deregulation, are key parts of the proposed policy mix and have the potential to support growth and the budding recovery in manufacturing.

Steady labor market provides support

Consumers are showing some signs of fatigue, suggesting that overall growth will moderate this year. However, we do not expect an abrupt pullback in personal consumption, as the factors driving it remain supportive. Wages continue to grow faster than the pace of inflation over the past 22 months, and unemployment remains historically low.

Government layoffs will apply some downward pressure on payroll growth, but federal employees account for only 2% of total employment. The private sector continues to add jobs at a healthy pace, above the 100,000–120,000 needed to keep pace with labor force growth and maintain a stable unemployment rate.

Action for investors

While the U.S. economy is downshifting, we expect the expansion to continue and recommend investors overweight equities over bonds. We view the Q1 pullback as an opportunity to deploy capital, rebalance and diversify.

Earnings estimates have come down from where they were in December 2024 but still forecast double-digit growth for the year.

Earnings estimates have come down from where they were in December 2024 but still forecast double-digit growth for the year.

Equity outlook

The U.S. equity market experienced its first correction in Q1, with the S&P 500 down 10.1% from peak to trough. Underneath the surface, there was a notable rotation out of the higher-valuation technology and growth sectors of the market to more defensive and cyclical sectors, including energy, health care and financials.

Market volatility to remain elevated

After two years of 20%-plus returns in the S&P 500, we would expect the pace of stock market gains to moderate in 2025, with volatility elevated. Policy uncertainty remains an overhang, with tariffs potentially weighing on consumer and corporate spending this year. These may be offset later this year with pro-growth policies, including tax reform and deregulation, although the structure of tariffs remains unknown.

We do not expect a deep or prolonged downturn

While a 20% drawdown could be likely, we would not expect markets to undergo a deep or prolonged bear market. These tend to occur when the U.S. economy is in or entering a recession or the Federal Reserve is raising interest rates aggressively. We don’t yet see these conditions in place for the year ahead, and thus investors can consider using pullbacks as opportunities.

Earnings growth is supportive of stocks

We continue to see solid corporate earnings growth in 2025, which should underpin stock market performance. Over the past quarter, earnings expectations have been revised lower, particularly for the first two quarters of the year, as companies have provided more conservative guidance given the uncertain policy backdrop. However, earnings estimates for the back half of the year have remained relatively stable, bringing full-year earnings growth forecasts to about 11%, which would mark a second year of double-digit corporate earnings growth.

In our view, if we get more certainty on the tariff regime in the months ahead and companies start to price in a more favorable tax and regulatory regime, some acceleration of growth in the back half of the year may be likely.

Action for investors

We view pullbacks as opportunities to rebalance, diversify and add quality investments to portfolios. We continue to favor cyclical sectors such as health care and financials, which are less exposed to tariff uncertainty, have more favorable valuations and may benefit from potential pro-growth policies.

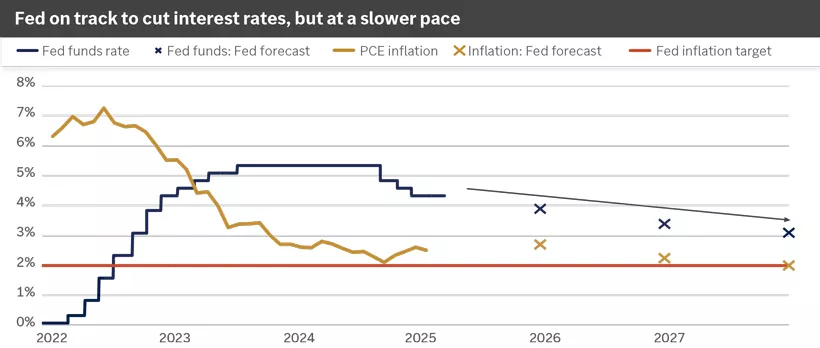

This chart shows the paths of the federal funds rate and PCE inflation since 2022, as well as forecasts for the fed funds rate and inflation past 2027. It also shows the Fed inflation target of 2%.

This chart shows the paths of the federal funds rate and PCE inflation since 2022, as well as forecasts for the fed funds rate and inflation past 2027. It also shows the Fed inflation target of 2%.

Fixed-income outlook

Solid fixed-income performance could continue as yields appear poised to remain range-bound, especially if the economy cools further. The Federal Reserve remains in an interest rate-cutting cycle, though the pace has slowed. Emerging-market debt could outperform U.S. high-yield bonds in this environment because of its higher credit quality and longer duration.

Bonds can help protect against slowing growth

A slowing economy can reduce demand for credit and loans, which, combined with Fed rate cuts, could drive yields lower. Bond prices — which move opposite interest rates — could benefit. Continued solid fixed-income performance can help support diversified portfolios.

Fed likely to stay on the sidelines for a while longer

The Fed has been on hold this year as it takes a more patient approach amid slowing disinflation and policy uncertainty. The Federal Open Market Committee (FOMC) released its updated economic projections in March, maintaining the fed funds rate “dot plot” at two rate cuts each for 2025 and 2026. The committee also cut its growth outlook and raised its inflation forecast.

The Fed slowed its balance-sheet reduction, known as quantitative tightening. This can ease monetary policy as the Fed will participate more actively in U.S. Treasury auctions, supporting bond prices and helping to contain yields to the upside. A resilient labor market and elevated inflation should allow the Fed to remain on hold as it awaits clarity on tariffs, potentially resuming rate cuts in June or July.

We favor emerging-market debt over U.S. high-yield bonds

Emerging-market debt appears attractive when compared to U.S. high-yield bonds, given its higher credit quality and interest rate sensitivity. Most emerging-market debt is investment-grade quality, which could make these bonds more resilient if the economy slows.

U.S. high-yield credit spreads — which reflect the excess yield above U.S. Treasury bonds to compensate for default risk — are well below their historical average. Any further slowing in the economy could drive credit spreads wider and bond prices lower.

Emerging-market debt also tends to have longer duration, which means it’s more sensitive to interest rates. It could benefit more from lower yields as major central banks likely continue easing monetary policy.

Action for investors

Bonds can help protect against a further slowdown in the economy as lower yields could drive bond prices higher. Consider raising allocations to emerging-market debt, if appropriate, with U.S. high-yield bonds as a potential source of funds.

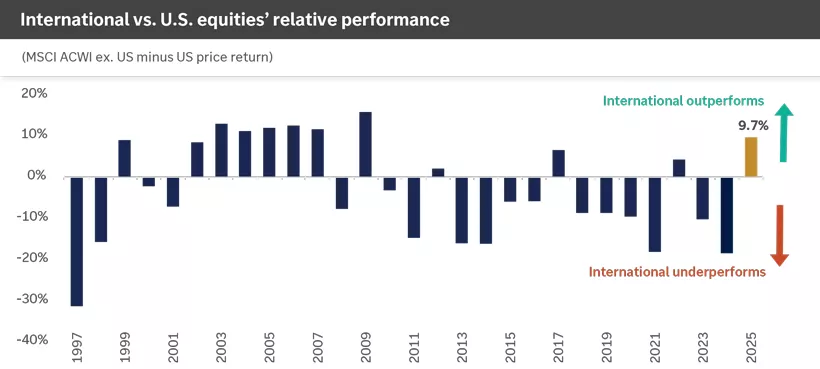

This chart shows the performance of the MSCI ACWI ex. US minus U.S. price return since 1997.

This chart shows the performance of the MSCI ACWI ex. US minus U.S. price return since 1997.

International outlook

After a long stretch of underperformance, international equities achieved their best yearly start (relative to U.S. equities) in the past 35 years. Diverging fiscal outlooks, a rotation to cheaper markets and a weaker dollar boosted returns. U.S. markets may retake the lead if sentiment around mega-cap tech stocks improves, but as Q1 showcased, international stocks play an important role in diversifying portfolios.

Germany pivots to higher fiscal spending

Over the past two years, eurozone growth has stagnated, with Germany, which accounts for 30% of the region’s gross domestic product (GDP), particularly hurt by a manufacturing slump. However, following elections in February, the German government approved a massive stimulus program to boost defense and infrastructure spending that is expected to inject €1 trillion of new spending over the next 10 years. This shifting attitude toward fiscal spending could improve the outlook for the country and the eurozone at a time when the U.S. is attempting to constrain government spending.

Investors rotate to cheaper markets

International equities have benefited from a rotation away from U.S. mega-cap technology companies and into investments that have lagged in the past. The Magnificent 7* companies have driven about half the gains of the S&P 500 over the past two years.

But increasing competition around AI, elevated valuations and accelerating earnings growth from cyclical sectors have triggered a change in market leadership that is favoring international indexes. The growth sectors (information technology, communication services and consumer discretionary) account for nearly 50% of the MSCI USA index versus 23% for the rest of the world and, as a result, are less of a drag when they fall out of favor.

Diversification is key amid trade uncertainty

Despite the improving outlook, the coast is not yet clear for overseas equities. An escalating trade war could weigh on global growth.

On the flip side, progress in negotiations and a potential rollback of the proposed tariffs would support the performance of overseas stocks. We think portfolio diversification will be critical for investors to navigate this year’s twists and turns.

Action for investors

We recommend overweighting U.S. stocks, staying neutral in emerging markets, and slightly underweighting international developed equities. If exposure to international equities is too low, we recommend rebalancing. Within fixed income, we see an opportunity to overweight emerging-market debt.

This chart shows the path of the U.S. Trade Policy Uncertainty Index, which was elevated in 2019 but is higher than that point now.

This chart shows the path of the U.S. Trade Policy Uncertainty Index, which was elevated in 2019 but is higher than that point now.

Higher policy uncertainty, but companies may adjust

Tariff policy — and the uncertainty around the size, scope and timing of potential tariffs — has weighed on stock market performance. This is largely because:

- Markets do not like uncertainty, and

- The potential impacts of tariffs could mean higher prices and lower consumption overall.

More clarity on tariffs may be coming

We expect to see more clarity on tariff policy in Q2. In our view, the administration may be taking a bifurcated approach to tariffs: Certain industries will be deemed critical, including steel and aluminum (for defense), semiconductors and perhaps autos and pharma, while new tariffs with key trading partners may be more of a basis for negotiation.

Once tariff policy is in place, there will be ongoing debate and adjustments, but consumers and corporations should have a better sense of the policy backdrop in which they are operating and can adjust accordingly. The hope is that policy focus will shift to a more pro-growth agenda that includes tax reform and deregulation, which could support better market sentiment overall.

Government cost-cutting could weigh on labor market, but impact limited

The headlines and actions around federal government layoffs and cost-cutting measures have put pressure on markets and consumer confidence broadly. Federal layoffs have totaled around 63,000 in the first two months of the year and could approach over 200,000 in the months ahead, in addition to perhaps around 450,000 government contractor layoffs, according to analysts.

While these cuts have weighed on local economies and households, the impact to the broader economy has been more limited. Federal government employees make up less than 2% of the total U.S. labor force. And with about 7.1 million people unemployed in the U.S., adding government layoffs to this figure could push the 4.1% unemployment rate toward 4.5%. This unemployment rate, however, is still well below the long-term U.S. average of about 5.7%.

Action for investors

Despite pullbacks, markets are supported by still-positive U.S. economic and earnings growth, alongside a resilient labor market. Don’t make investment decisions based on policy uncertainty or political headlines, and instead focus on long-term investments in quality, diversified portfolios across sectors, asset classes and regions.

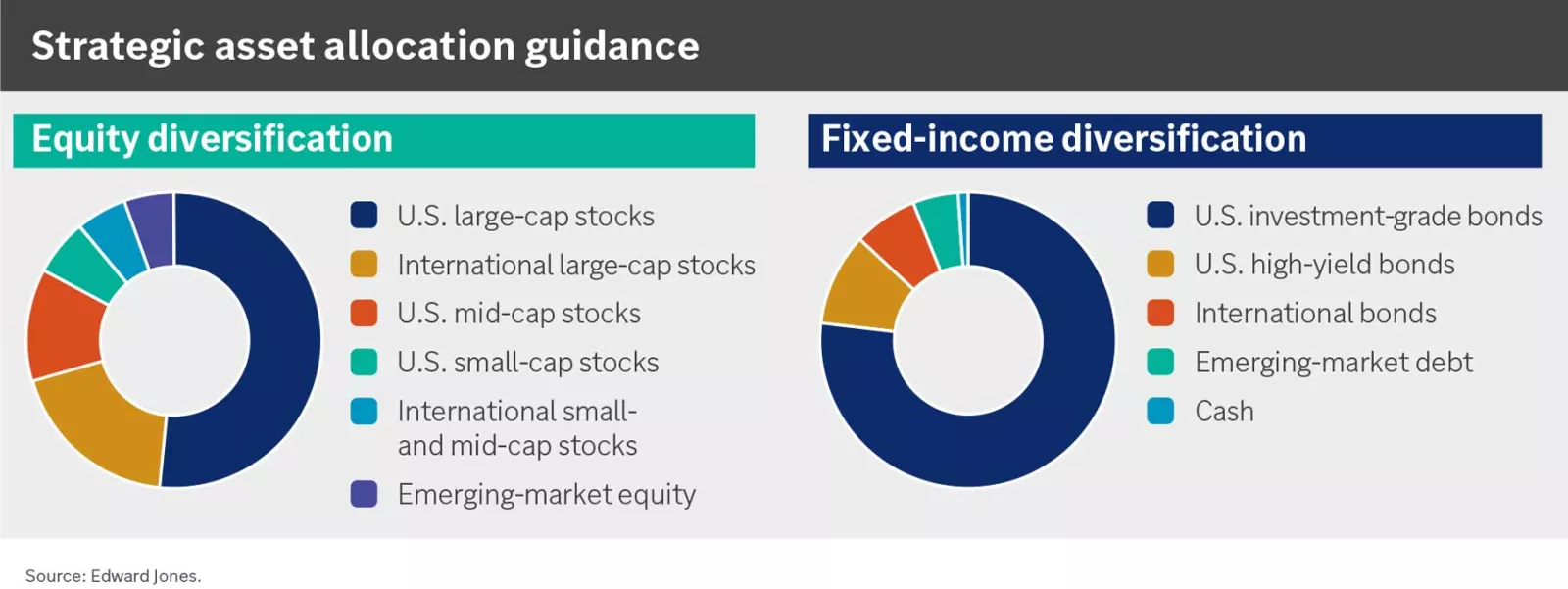

Strategic asset allocation guidance

Our strategic asset allocation represents our view of balanced diversification for the fixed-income and equity portions of a well-diversified portfolio, based on our outlook for the economy and markets over the next 30 years. The exact weightings (neutral weights) to each asset class will depend on the broad allocation to equity and fixed-income investments that most closely aligns with your comfort with risk and financial goals.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Within our strategic guidance, we recommend these asset classes:

Equity diversification: U.S. large-cap stocks, international large-cap stocks, U.S. mid-cap stocks, U.S. small-cap stocks, international small- and mid-cap stocks, emerging-market equity.

Fixed-income diversification: U.S. investment-grade bonds, U.S. high-yield bonds, international bonds, emerging-market debt, cash.

Opportunistic portfolio guidance

Our opportunistic portfolio guidance represents our timely investment advice based on our global outlook. We expect this guidance to enhance your portfolio’s return potential, relative to our long-term strategic portfolio guidance, without taking on unintentional risk.

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks and U.S. mid-cap stocks; neutral for U.S. small-cap stocks and emerging-market equity; underweight for international large-cap stocks and international small- and mid-cap stocks.

Fixed income — underweight overall; overweight for emerging-market debt; neutral for U.S. investment-grade bonds and cash; underweight for U.S. high-yield bonds and international bonds.

Our opportunistic asset allocation guidance follows:

Equity — overweight overall; overweight for U.S. large-cap stocks and U.S. mid-cap stocks; neutral for U.S. small-cap stocks and emerging-market equity; underweight for international large-cap stocks and international small- and mid-cap stocks.

Fixed income — underweight overall; overweight for emerging-market debt; neutral for U.S. investment-grade bonds and cash; underweight for U.S. high-yield bonds and international bonds.

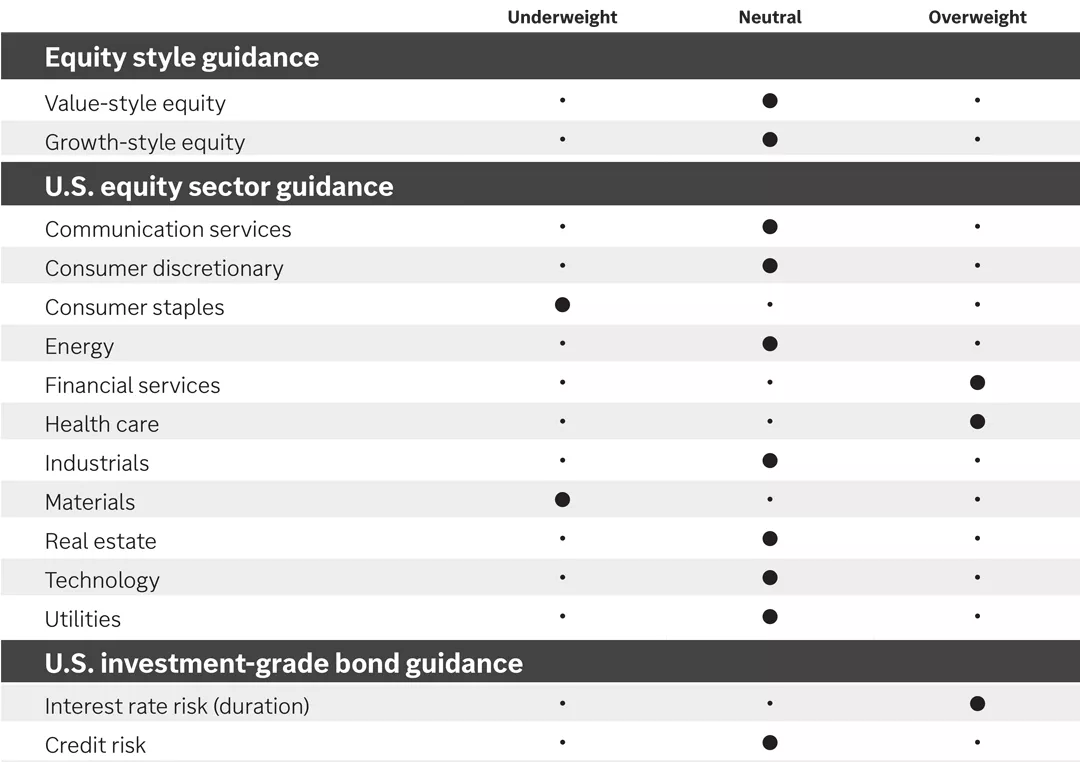

Our opportunistic guidance follows:

Equity style guidance: Neutral for value-style equity and growth-style equity.

U.S. equity sector guidance: Overweight for financial services and health care; neutral for communications services, consumer discretionary, energy, industrials, real estate, technology and utilities; underweight for consumer staples and materials.

U.S. investment-grade bond guidance: Overweight in interest rate risk (duration); neutral in credit risk.

Our opportunistic guidance follows:

Equity style guidance: Neutral for value-style equity and growth-style equity.

U.S. equity sector guidance: Overweight for financial services and health care; neutral for communications services, consumer discretionary, energy, industrials, real estate, technology and utilities; underweight for consumer staples and materials.

U.S. investment-grade bond guidance: Overweight in interest rate risk (duration); neutral in credit risk.

Visit our monthly portfolio brief for a discussion of portfolio performance.

Investment performance benchmarks

It’s natural to compare your portfolio’s performance to market performance benchmarks, but it’s important to put this information in the right context and understand the mix of investments you own. Talk with your financial advisor about any next steps for your portfolio to help you stay on track toward your long-term goals.

Asset class performance

As of March 31, 2025

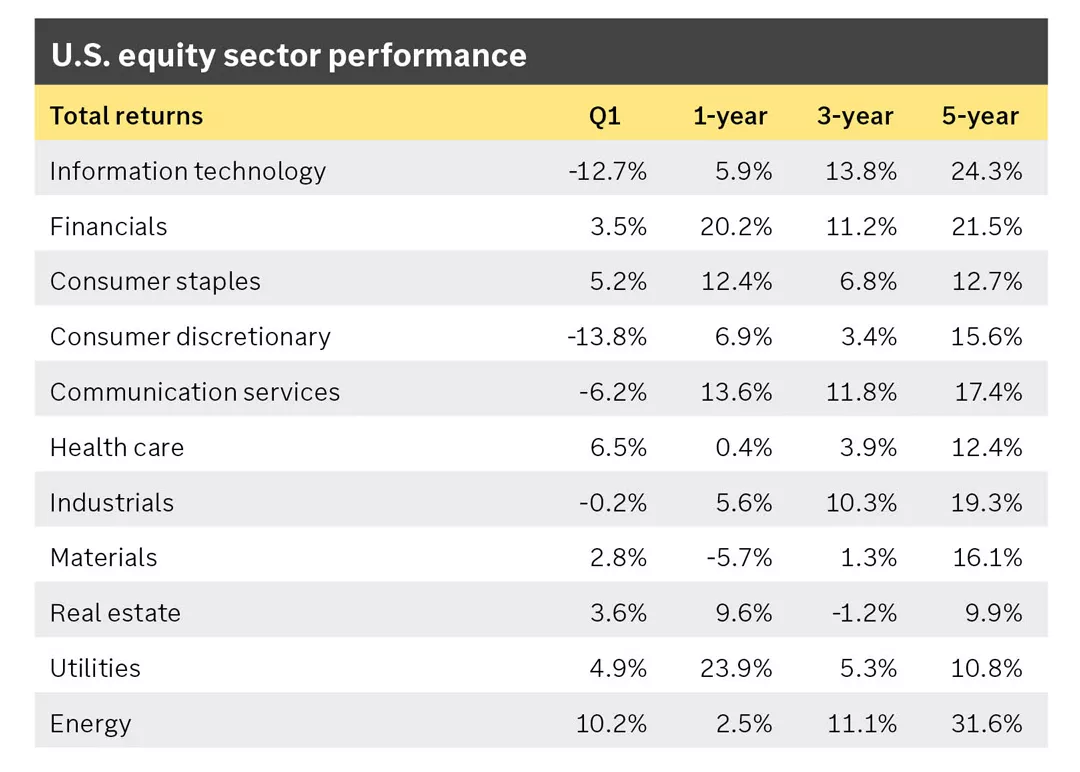

U.S. equity sector performance

The above tables compare first-quarter performance in varying asset classes and stock market sectors with three- and five-year returns. Among asset classes, U.S. large-cap stocks fell 4.3% in the first quarter, U.S. mid-cap stocks fell 3.4%, U.S. small-cap stocks fell 9.5%, international developed large-cap stocks rose 6.9%, international small- and mid-cap stocks rose 5%, emerging-market stocks rose 2.9%, U.S. investment-grade bonds rose 2.8%, international bonds fell 0.2%, emerging-market debt rose 2.3%, U.S. high-yield bonds rose 1%, and cash rose 1%.

In stock market sectors, information technology fell 12.7% in the first quarter, financials rose 3.5%, consumer staples rose 5.2%, consumer discretionary fell 13.8%, communication services fell 6.2%, health care rose 6.5%, industrials fell 0.2%, materials rose 2.8%, real estate rose 3.6%, utilities rose 4.9%, and energy rose 10.2%.

The above tables compare first-quarter performance in varying asset classes and stock market sectors with three- and five-year returns. Among asset classes, U.S. large-cap stocks fell 4.3% in the first quarter, U.S. mid-cap stocks fell 3.4%, U.S. small-cap stocks fell 9.5%, international developed large-cap stocks rose 6.9%, international small- and mid-cap stocks rose 5%, emerging-market stocks rose 2.9%, U.S. investment-grade bonds rose 2.8%, international bonds fell 0.2%, emerging-market debt rose 2.3%, U.S. high-yield bonds rose 1%, and cash rose 1%.

In stock market sectors, information technology fell 12.7% in the first quarter, financials rose 3.5%, consumer staples rose 5.2%, consumer discretionary fell 13.8%, communication services fell 6.2%, health care rose 6.5%, industrials fell 0.2%, materials rose 2.8%, real estate rose 3.6%, utilities rose 4.9%, and energy rose 10.2%.

Investment Policy Committee

The Investment Policy Committee (IPC) defines and upholds Edward Jones investment philosophy, which is grounded in the principles of quality, diversification and a long-term focus.

The IPC meets regularly to talk about the markets, the economy and the current environment, propose new policies and review existing guidance — all with your financial needs at the center.

The IPC members — experts in economics, market strategy, asset allocation and financial solutions — each bring a unique perspective to developing recommendations that can help you achieve your financial goals.

*Apple, Microsoft, Amazon, Alphabet, Meta, Nvidia and Tesla.

Diversification does not ensure a profit or protect against loss in a declining market.

Rebalancing may result in a taxable event.

Understand the risks involved in owing investments, including interest rate risk, credit risk and market risk. The value of investments fluctuates, and investors can lose some or all of their principal. Special risks are inherent in international and emerging-market investing, including those related to currency fluctuations and foreign political and economic events.

Investing in bonds involves risks, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and investors can lose principal value if the investment is sold prior to maturity. Emerging-market securities can be more volatile than securities in developed countries. Currency and political risks are accentuated in emerging markets.

Past performance is not a guarantee of future results.

This content is provided as general information only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.