Monthly fixed-income focus

Bonds can continue to perform well even with the Fed on hold

What you need to know

- Solid fixed-income performance could continue as yields appear poised to remain range-bound, especially if the economy cools further.

- The Federal Reserve remains in its rate-cutting cycle, though the pace has slowed.

- Emerging-market debt could outperform U.S. high-yield bonds in this environment because of its higher credit quality and longer duration.

Portfolio tip

Bonds can help protect against a further slowdown in the economy as lower yields could drive bond prices higher. Consider raising allocations to emerging-market debt, if appropriate, with U.S. high-yield bonds as a potential source of funds.

Bonds can help protect against slowing growth

A slowing economy can reduce demand for credit and loans, which, combined with Fed interest rate cuts, could drive yields lower. Bond prices — which move inversely to interest rates — could benefit. Continued solid fixed-income performance can help support diversified portfolios.

Fed likely to stay on the sidelines for a while longer

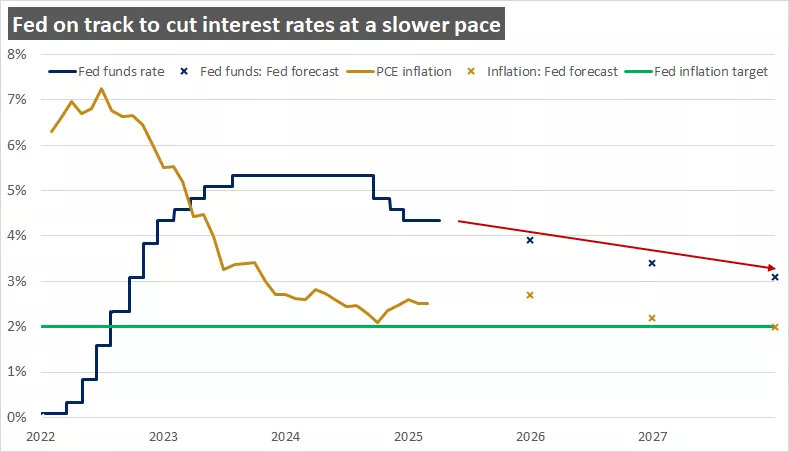

The Fed has been on hold this year as it takes a more patient approach amid slowing disinflation and policy uncertainty. The Federal Open Market Committee (FOMC) released its updated economic projections in March, maintaining the fed funds rate “dot plot” at two rate cuts each for 2025 and 2026. The committee also cut its growth outlook and raised its forecast for Personal Consumption Expenditure (PCE) inflation.1 The Fed slowed its balance-sheet reduction, known as quantitative tightening. This can ease monetary policy as the Fed will participate more actively in U.S. Treasury auctions, supporting bond prices and helping to contain yields to the upside. A resilient labor market and elevated inflation should allow the Fed to remain on hold as it awaits clarity on tariffs, potentially resuming rate cuts in June or July.

This chart shows the path of the fed funds rate and PCE inflation since 2022 and Fed forecasts through 2027.

This chart shows the path of the fed funds rate and PCE inflation since 2022 and Fed forecasts through 2027.

We favor emerging-market debt over U.S. high-yield bonds

Emerging-market debt appears attractive when compared to U.S. high-yield bonds, given its higher credit quality and interest rate sensitivity.2 Most emerging-market debt is investment-grade quality, which could make these bonds more resilient if the economy slows. U.S. high-yield credit spreads — which reflect the excess yield above U.S. Treasury bonds to compensate for default risk — are well below their historical average.2 Any further slowing in the economy could drive credit spreads wider and bond prices lower. Emerging-market debt also tends to have longer duration, which means it’s more sensitive to interest rates. It could benefit more from lower yields as major central banks likely continue easing monetary policy.

Brian Therien

Brian Therien is a Senior Fixed Income Analyst on the Investment Strategy team. He analyzes fixed-income markets and products, and develops advice and guidance to help clients achieve their long-term financial goals.

Brian earned a bachelor’s degree in finance from the University of Illinois at Urbana–Champaign, graduating with honors. He received his MBA from the University of Chicago Booth School of Business.

Important information:

1 U.S. Federal Reserve

2 Bloomberg

This content is for educational and informational purposes only and should not be interpreted as specific investment advice. Investors should make investment decisions based on their unique investment objectives and financial situation.

Past performance of the markets is not a guarantee of future results.

Before investing in bonds, you should understand the risks involved, including credit risk and market risk. Bond investments are also subject to interest rate risk such that when interest rates rise, the prices of bonds can decrease, and the investor can lose principal value if the investment is sold prior to maturity.

Diversification does not guarantee a profit or protect against loss in declining markets.