Types of Retirement Accounts

We offer many types of retirement accounts and can help you understand the differences, so you can choose what makes the most sense for your financial goals and investing strategy.

View Retirement Accounts

When it comes to growing your retirement assets, time can be a valuable tool.

Not only does it matter how early you start putting money aside for retirement, but delaying your retirement date by just a couple of years — and postponing the time you begin receiving Social Security benefits — can also have a significant impact on your retirement income.

This is good news for Americans, who, thanks to advances in medicine and healthier lifestyles, are living longer in retirement, meaning their investments may need to last 25 to 30 years or more. American men at age 65 can expect about 20 more years of life, on average, and women can expect to live almost 22 more years, according to the Society of Actuaries. This means that half of the 65-year-old population is likely to live beyond these averages, with almost 30% of 65-year-old men and 40% of 65-year-old women likely to reach age 90.

What’s more, traditional attitudes about retirement are changing, with a greater share of older Americans remaining in the workforce. Doing so helps them feel more connected socially, and it improves their mental and physical well-being by giving them a sense of purpose.

Here are three reasons why you could benefit from retiring later.

A significant challenge retirees face is making their retirement savings last long enough to sustain them throughout their retirement.

A study by the National Bureau of Economic Research found that working three to six months longer can result in an increase in retirement income that’s equivalent to boosting your retirement contributions by as much as 1% over 30 years of employment.

The study also notes that the benefits of traditional retirement strategies — such as putting more of your income toward savings or switching to a low-cost portfolio — diminish as you get closer to retirement.

Working longer and delaying the time you start to draw on your retirement funds could dramatically improve your retirement lifestyle, providing you with more time to save and earn a return on your investments.

It’s possible to start collecting your Social Security benefits at age 62, but the earlier you start, the smaller your checks will be.

It actually pays to delay taking Social Security to a date later than your full retirement age (FRA) because you can accrue credits that boost your benefits. You get 8% more for each year you delay claiming beyond your FRA, up to age 70.

But remember: Those credits come to an end when you hit 70, so waiting longer won’t bring you higher benefits and could mean you miss out on some payments.

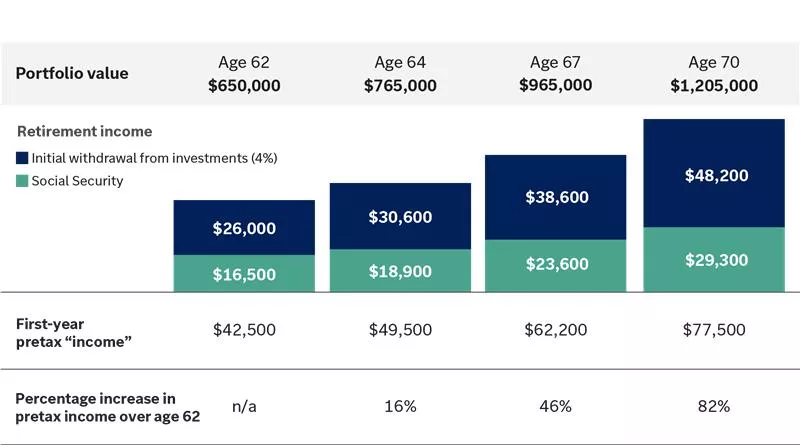

The chart below shows how delaying retirement by a few years could increase your Social Security benefits.

The above chart demonstrates the potential benefits of waiting to retire by showing the increase in value of one's investment portfolio and first-year pretax retirement income over time.

The smallest bar shows that with a portfolio of $650,000 at age 62, one's first-year pretax retirement income would be $42,500 with $16,500 coming from Social Security benefits and $26,000 withdrawn from their portfolio. The next bar shows that the portfolio would grow to $765,000 by age 64, resulting in a first-year pretax income of $49,500 with $18,900 coming from Social Security benefits and $30,600 withdrawn from their portfolio. This represents a 16% increase in pretax income over age 62. The next bar shows that the portfolio would grow to $965,000 by age 67, resulting in a first-year pretax income of $62,200 with $23,600 coming from Social Security benefits and $38,600 withdrawn from their portfolio. This represents a 46% increase in pretax income over age 62. The final bar shows that the portfolio would grow to $1,205,000 by age 70, resulting in a first-year pretax income of $77,500 with $29,300 coming from Social Security benefits and $48,200 withdrawn from their portfolio. This represents an 82% increase in pretax income over age 62.

The above chart demonstrates the potential benefits of waiting to retire by showing the increase in value of one's investment portfolio and first-year pretax retirement income over time.

The smallest bar shows that with a portfolio of $650,000 at age 62, one's first-year pretax retirement income would be $42,500 with $16,500 coming from Social Security benefits and $26,000 withdrawn from their portfolio. The next bar shows that the portfolio would grow to $765,000 by age 64, resulting in a first-year pretax income of $49,500 with $18,900 coming from Social Security benefits and $30,600 withdrawn from their portfolio. This represents a 16% increase in pretax income over age 62. The next bar shows that the portfolio would grow to $965,000 by age 67, resulting in a first-year pretax income of $62,200 with $23,600 coming from Social Security benefits and $38,600 withdrawn from their portfolio. This represents a 46% increase in pretax income over age 62. The final bar shows that the portfolio would grow to $1,205,000 by age 70, resulting in a first-year pretax income of $77,500 with $29,300 coming from Social Security benefits and $48,200 withdrawn from their portfolio. This represents an 82% increase in pretax income over age 62.

The decisions you make about claiming Social Security can have a big impact on your retirement income. In fact, we’ve identified four key factors that could influence your decision on when to take your benefits.

To see where you currently stand, your yearly statement from the Social Security Administration can provide you with an estimate of your retirement benefit, which is based on your FRA and work history.

Instead of the rather low-key retirements of their parents, today’s retirees want to be “more active, engaged, exploratory and purposeful in retirement,” according to research conducted by Edward Jones and Age Wave, an organization focused on aging and retirement.

This new attitude toward retirement means it no longer represents the end of work for many, but instead is seen as an opportunity to enjoy greater freedoms, such as choosing whether and how much they want to work.

More retirees are working on their own terms, often with renewed purpose, the research finds. One-third of those planning to retire say they are interested in working in some capacity in retirement. And two-thirds of workers age 65 and older say they work primarily because they want to, not because they have to.

Continuing to work helps retirees maintain social interactions and regularly exercise their mental abilities, potentially reducing their risk of cognitive decline.

Want to learn more about improving your retirement income? Talk to your Edward Jones financial advisor about steps you can take now to control what your income looks like in the future.

We offer many types of retirement accounts and can help you understand the differences, so you can choose what makes the most sense for your financial goals and investing strategy.

View Retirement Accounts

3 things you can do now to help reduce your future tax bill

View Tax Diversification Strategies in Retirement

Preparing for retirement can come with plenty of what-ifs that could impact your plan. Learn more about big retirement risks to look out for.

Learn MoreImportant information:

Content is provided as educational only and should not be relied on for other than broadly informational purposes. Investors should make investment decisions based on their unique investment objectives and financial situation.