Making the switch from saving to spending in retirement

You likely prepared years for this. But, now that you're retired, it may be hard to go from saving to spending mode. Here are five tips to consider when making the switch from saving to spending.

1. Know your budget

Your retirement strategy likely assumes you're spending a certain amount each year. If you're actual spending is higher than what your strategy assumes, you increase the risk of running out of money in retirement. Be sure to understand your monthly budget and regularly review your spending to ensure you're staying within your means. Don't forget to set aside what you may need for annual expenses such as taxes and insurance.

2. Separate your spending assets

Separating your spending assets from your other investments will make it easier to see exactly what you have available for spending. While the accounts and investments you use to "refill" your spending account may vary from year to year, as a general guide, we recommend the following sequence:

- Nonportfolio sources such as Social Security (if already claiming) and pensions/lifetime annuities (if applicable)

- Required minimum distributions (RMDs) from retirement accounts (if applicable)

- Dividends and interest from taxable accounts (including municipal bond interest)

- Sales from your investments, starting with taxable accounts, followed by traditional retirement accounts and, finally, Roth retirement accounts

3. Maintain an appropriate allocation to cash and short-term fixed income

We generally recommend retirees maintain 12 months' worth of portfolio withdrawals in cash in their separate spending account and another three to five years of portfolio withdrawals in a short-term, fixed-income ladder. Maintaining appropriate cash reserves can help ensure your retirement spending needs are met, while allowing your stocks more time to recover following a market decline. Keep in mind, though, that owning too much cash and short-term fixed income also comes with risks, and that is that your portfolio doesn't earn enough to keep up with inflation. We believe a more balanced allocation between equities and fixed income is key.

4. Consider an annuity

An annuity* can provide a guaranteed income stream for life, regardless of how the market performs or how long you live, which may give you greater comfort with spending. While annuities are often purchased ahead of retirement, depending on the type of annuity, your age and your life expectancy, one still may make sense for your situation.

5. Review your strategy regularly and be flexible

Your retirement could be 25 years or longer, and as much as you've prepared, a lot can change along the way. That's why it's important to review your strategy, including your preparedness for potential risks, at least annually or sooner if you experience a life event.

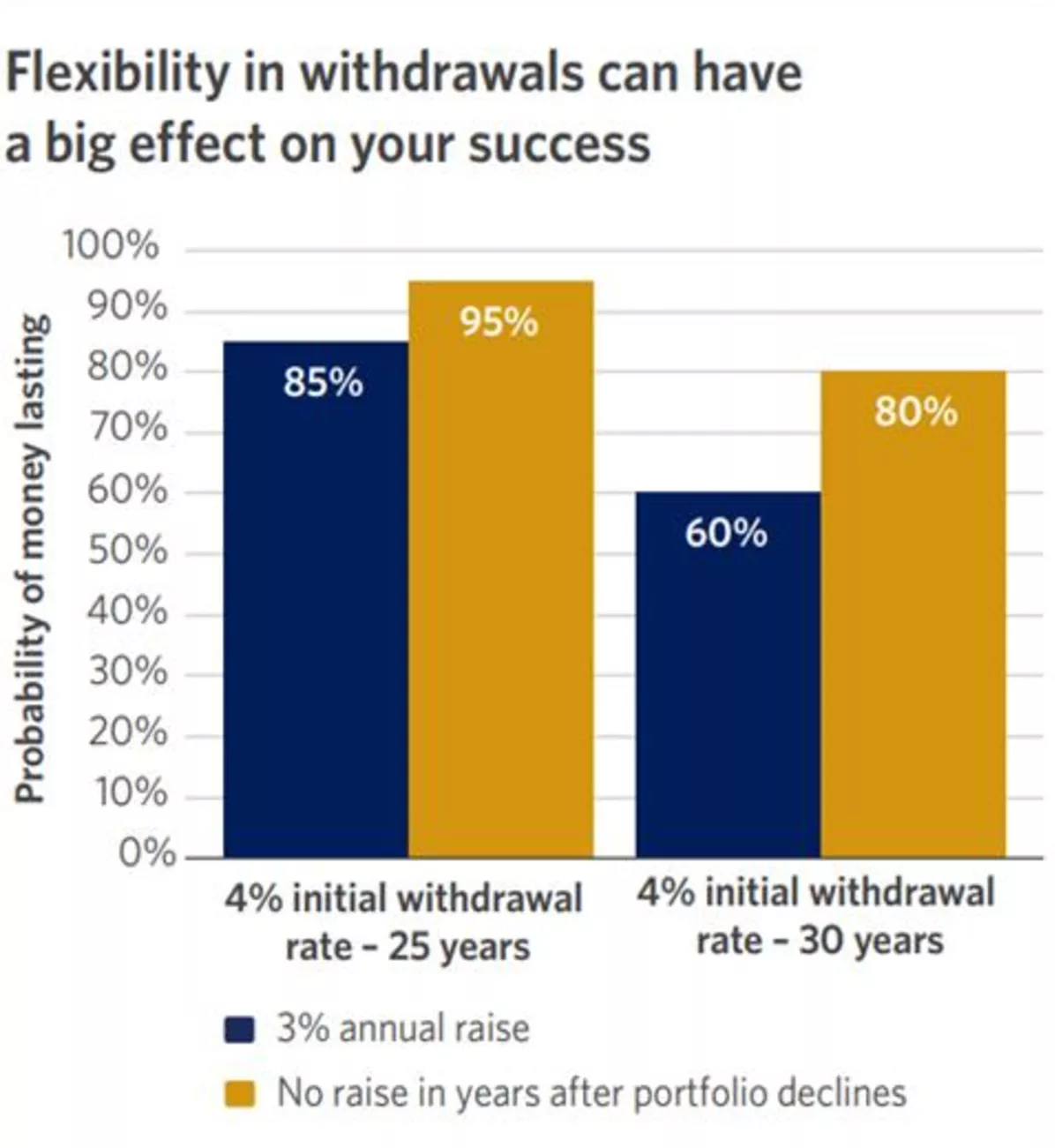

You may also have to be flexible with your strategy in retirement to help ensure your money lasts. Even minor adjustments can have a dramatic effect on your portfolio's longevity. The following chart compares two different spending patterns: one increases withdrawals by 3% every year regardless of portfolio performance, while the other only increases spending by 3% in years following a portfolio increase and takes no raises in years following a portfolio decline.

income/50% stocks portfolio, rebalanced annually. The portfolio includes cash (1%),

U.S. investment-grade bonds (39%), U.S. high-yield bonds (10%), U.S. large-cap stocks

(33%), and international large-cap stocks (17%). Expected returns based on long-term

capital market expectations for cash of 2.9%, U.S. bonds of 3.6% to 6.0%, U.S. large-cap

stocks of 6.8%, and international large-cap stocks of 7.6%. We also assume an annual fee

of 1%. This hypothetical example is for illustrative purposes only and does not reflect the

performance of a specific investment. Values rounded to the nearest 5%.

The bar farthest to the left shows the probability of your money lasting for 25 years is 85% if you take a 4% initial withdrawal and increase your withdrawal by 3% each year. The next bar shows the probability of your money lasting 25 years increases to 95% if you take the same starting withdrawal but do not increase the withdrawal amount in years after the portfolio declines. The third bar from the left shows the probability of your money lasting 30 years is 60% if you take a 4% initial withdrawal and increase your withdrawal by 3% each year. The last bar shows the probability of your money lasting 30 years increases to 80% if you take the same starting withdrawal but do not increase the withdrawal amount in years after the portfolio declines.

income/50% stocks portfolio, rebalanced annually. The portfolio includes cash (1%),

U.S. investment-grade bonds (39%), U.S. high-yield bonds (10%), U.S. large-cap stocks

(33%), and international large-cap stocks (17%). Expected returns based on long-term

capital market expectations for cash of 2.9%, U.S. bonds of 3.6% to 6.0%, U.S. large-cap

stocks of 6.8%, and international large-cap stocks of 7.6%. We also assume an annual fee

of 1%. This hypothetical example is for illustrative purposes only and does not reflect the

performance of a specific investment. Values rounded to the nearest 5%.

The bar farthest to the left shows the probability of your money lasting for 25 years is 85% if you take a 4% initial withdrawal and increase your withdrawal by 3% each year. The next bar shows the probability of your money lasting 25 years increases to 95% if you take the same starting withdrawal but do not increase the withdrawal amount in years after the portfolio declines. The third bar from the left shows the probability of your money lasting 30 years is 60% if you take a 4% initial withdrawal and increase your withdrawal by 3% each year. The last bar shows the probability of your money lasting 30 years increases to 80% if you take the same starting withdrawal but do not increase the withdrawal amount in years after the portfolio declines.

Not yet retired?

If you're not yet retired, here are some additional strategies to help ensure your savings last you through retirement.

How we can help

Talk to your Edward Jones financial advisor today about ways to help make your money last as you make the switch from saving to spending.

Important information:

*Annuities are long-term investments designed to provide tax-deferred savings for and during

retirement. Annuity guarantees are subject to the claims paying ability of the issuing life insurance company.

This content is provided as educational only and should not be interpreted as specific investment advice.

Investors should make investment decisions based on their unique investment objectives and financial

situation.